Jak vyplnit PPD

Pokladní dokladyHlavička PPD – název (Příjmový pokladní doklad), Organizace (většinou firmy dávají razítko, kde jsou náležitosti jako: název obchodní firmy, adresa, IČO a DIČ); číslo dokladu, datum a přílohy)Přijato od (jméno, adresa) – adresa firmy, živnostníka nebo jakékoli jiné osoby, která nám platí

Archiv

Co je to příjmový pokladní doklad

Příjmový pokladní doklad je dokladem o prodeji zboží či poskytnutí služeb za hotové nebo se vystavuje jako potvrzení o úhradě faktury v hotovosti.

Jak Zauctovat prebytek materialu

Přebytky materiálu účtujeme do výnosů na účet 648 Účet 648 – Ostatní provozní výnosy (Výnosový – daňový) 648 Jiné provozní výnosy.

Jak poznat Má dáti dál

Jestli máte alespoň základní znalosti účetnictví, pak nejspíš víte, že levá strana účtu se v odborné terminologii nazývá „Má dáti“ a pravá strana účtu „Dal“. Často se zapisují pomocí jednoduchých zkratek – MD a D. To asi víte taky.

Kdy se vystavuje paragon

K původnímu dotazu: Termín paragon ani faktura není v žádném zákonu definován. Paragon, účtenka nebo zjednodušený daňový doklad se vystavují při platbě v hotovosti. Faktura se vystavuje tehdy, pokud je domluveno, že zákazník zaplatí v budoucnu, ať už převodem z účtu nebo hotově.

Kdo podepisuje příjmový pokladní doklad

Originál s podpisem příjemce dostává ten, kdo platí, protože je to jeho doklad o zaplacení. Příjemce v podstatě doklad nepotřebuje, nikdo asi nebude zpochybňovat, že peníze přijal, pokud to bude tvrdit.

Kdy použít příjmový pokladní doklad

Příjmový pokladní doklad (zkráceně jen PPD) je doklad o příjmu peněz do pokladny nebo o platbě kartou a lze vystavit na fakturu nebo zálohovou fakturu. Slouží pro úhradu částky do pokladny – tedy platba v hotovosti nebo platba kartou.

Jak má vypadat příjmový doklad

Je povinné uvést označení dokladu (číslo), identifikaci příjemce a plátce, uvést datum vyhotovení dokladu, datum platby (pokud není shodný s datem vyhotovení), peněžní částku, účel platby a doklad musí být podepsán odpovědnou osobou za účetní případ a zaúčtování.

Jak se účtuje přebytek

Přebytek účtujeme v 6. účtové třídě – ve výnosech a zároveň jako přírůstek na vhodném účtu (pokladna, bankovní účet, zásoby atd.). Obvykle se pro jejich účtování používá 68. účtová skupina a účet Mimořádné výnosy.

Co je to manko

Situace, kdy je skutečný stav vyšší než stav účetní, se označuje jako přebytek. Situace, kdy je skutečný stav nižší než stav v účetnictví, se označuje jako manko (v případě hotovosti a cenin jako schodek).

Jak účtovat má dáti dál

U faktury vystavené účtujete vždy na účet 311 – Odběratelé v celkové částce na stranu MÁ DÁTI. Na stranu DAL budete účtovat vždy buď výnosový účet (311/6xx), nebo výnosy příštích období.

Co se účtuje na 604

Poskytované slevy odběratelům se účtují v průběhu účetního období na účet 604 v okamžiku poskytnutí slevy. Při poskytnutí slev v jiném účetním období je nutné provést časové rozlišení těchto slev do období, kdy došlo k prodeji a tím i zaúčtování prodaného zboží.

Jak účtovat paragon

Zjednodušené daňové doklady (paragony) se zadávají do agendy Účetnictví/Pokladna. Vzhledem k tomu, že na těchto dokladech je vyčíslena pouze celková hodnota a sazba DPH bez uvedení DPH v korunové hodnotě, je nutné uvést celkovou hodnotu dokladu v příslušné sazbě DPH do třetího sloupce sekce Částka.

Co vše musí být na Uctence

EET účtenka musí obsahovat:fiskální identifikační kód (nebo podpisový kód pokladny, pokud zrovna nejde internet)bezpečnostní kód poplatníka.označení provozovny, v níž je tržba uskutečněna.označení pokladního zařízení, na němž je tržba evidována.pořadové číslo účtenky.

Kdy musím vystavit příjmový pokladní doklad

Příjmový pokladní doklad vystavujete, pokud do pokladny přijímáte peníze (např. lidé u vás nakupují). Výdajový pokladní doklad vystavujete, pokud z pokladny peníze vydáváte (vy nakupujete).

Kdy stačí Paragon

Více o pokladních dokladech se dozvíte zde. Od faktury pak zjednodušený daňový doklad (paragon) odlišuje především moment uhrazení. Paragon zpravidla vystavujete, když od zákazníka přebíráte peníze osobně, transakce je tedy už dokončená. Zatímco v případě platby na fakturu dostanete peníze až později.

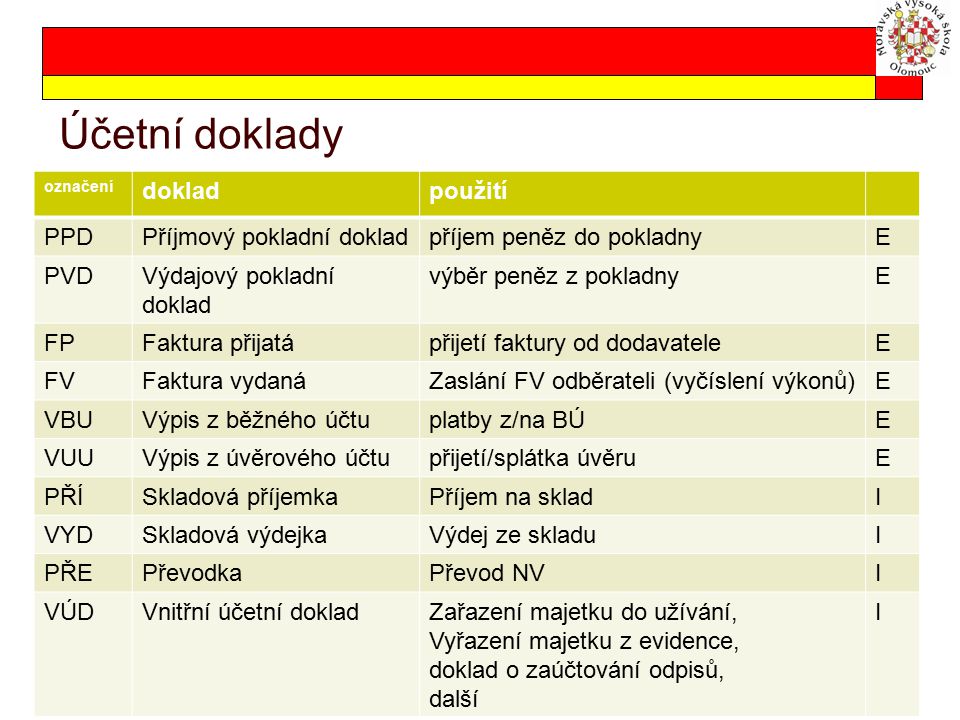

Jak Delime ucetni doklady

Účetní doklady se člení dle druhu na:faktury (přijaté a vystavené),pokladní doklady (příjmové a výdajové),bankovní výpisy,interní (příjemky, výdejky, výplatní listiny apod.).

Kdo je osoba odpovědná za účetní případ

V případě, že by se jednalo o účetní jednotku bez právní subjektivity, odpovídá za vedení jejího účetnictví včetně sestavení účetní závěrky osoba, které je uloženo sestavit účetní závěrku a osoba jednající jménem účetní jednotky. Nebo to může být také osoba stanovená na základě zvláštního právního předpisu.

Kdy se provádí inventarizace

Inventarizace se provádí k okamžiku, kdy účetní jednotka sestavuje řádnou nebo mimořádnou účetní závěrku. Alespoň jednou za účetní období se musí provést průběžná inventarizace, ale pouze u zásob, které jsou účtovány dle druhů a u hmotného movitého majetku, který nemá jasně dané místo, kam náleží.

Jak účtovat Maňka a škody

Manka a škody vzniklé na finančním majetku se účtují jako finanční náklady (účet 569-Manka a škody na finančním majetku). Způsobený úbytek majetku může být rovněž kompenzován náhradou od pojišťovny, je-li účetní jednotka pojištěna, nebo může být vymáhán na odpovědných osobách.

Co se účtuje na účet 351

2023. Účet 351-Pohledávky – ovládaná nebo ovládající osoba je určen k zachycení takových pohledávek za ovládanými a ovládajícími osobami, mezi ovládanými a ovládajícími osobami a za ovládajícími a ovládanými osobami, které nevznikly na základě obchodního vztahu.

Co se účtuje na 601

Na tento účet se účtují tržby za hotové výrobky, popř. za polotovary nebo nedokončenou výrobu, pokud by došlo k jejich prodeji dříve, než se stanou výrobkem.

Co se účtuje na 395

Účet 395 používáme jako spojovací pro převod materiálu mezi sklady. Konkrétně: výdejka z jednoho skladu 39541/11210 a příjemka na druhý sklad 11222/39541. Na konci roku se nám stalo, že výdejka vznikla 12/2017, ale příjem udělali až 01/2018.

Co je to DPH na vstupu

DPH na vstupu – DPH, které zaplatíte spolu s přijatým zbožím, materiálem, službou, dlouhodobým majetkem. Doklad k DPH na vstupu je nejčastěji faktura přijatá, splátkový kalendář nebo přijaté paragony. Vůči finančnímu úřadu vykazujete DPH na vstupu jako pohledávku.

Jak zaúčtovat fakturu od plátce DPH

Přijaté faktury pak účtujete vždy na účet 321 – Dodavatelé závazky z obchodních vztahů. Plátci DPH na tento účet účtují i daň. Evidenci a uchování přijatých faktur vám nařizuje zákon o účetnictví. Pokud to neuděláte, budete mít problém při případné kontrole z finančního úřadu.