Co tvoří vlastní kapitál

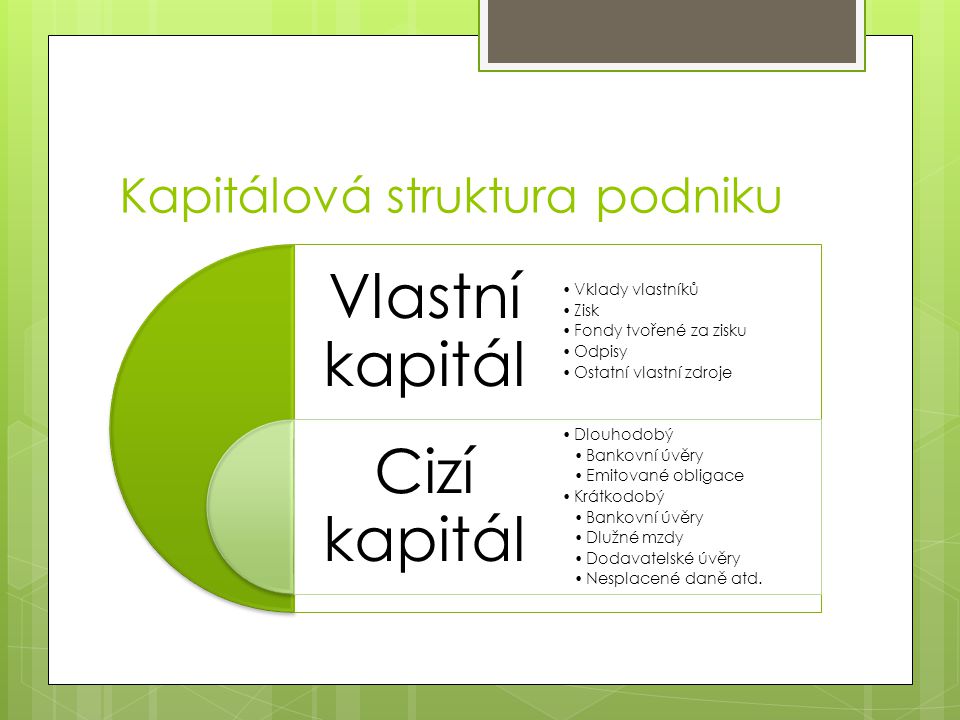

Vlastní kapitál tak zahrnuje peněžité a nepeněžité vklady majetku do firmy, kapitálové fondy, hospodářské výsledky z minulých účetních období i z období současného a fondy tvořené ze zisku (rezervní fond). V rozvaze se vykazuje na straně pasiv.

Co jsou náklady na vlastní kapitál

Náklady kmenového kapitálu lze definovat jako výnosnost kmenových akcií, kterou požaduje investor od těchto akcií. Také s emisí kmenových akcií jsou spojeny emisní náklady.

Co se počítá do základního kapitálu

Základní kapitál (ZK) je součástí vlastního kapitálu společnosti a představuje hodnotu vkladů jednotlivých vlastníků do nově vznikající firmy. Tyto vklady do s.r.o. mohou být: peněžité (hotovost nebo peníze na bankovních účtech) nepeněžité (movité a nemovité věci oceněné znaleckým posudkem).

Archiv

Jak se počítá vlastní kapitál

Vlastní kapitál (equity) je celková hodnota podniku, která patří jeho majitelům. Zjistí se jednoduše odečtením cizího kapitálu (dluhy, závazky a další) od celkových aktiv.

Archiv

Co je to kapitál

Co je kapitál Kapitálem rozumíme vše, co vynakládáme na to, aby vznikly další hodnoty. Vůbec nejjednodušší definice kapitálu říká, že jsou to peníze, které přinášejí další peníze. Kapitál obecně jsou dříve vytvořené prostředky, které se nespotřebují, ale použijí jako vstup do další výroby pro dosažení budoucího zisku.

Jak se účtuje základní kapitál

O základním kapitálu budeme účtovat ve skupině 41 (obvykle na účtu 411). Na oddělených analytických účtech je potřeba sledovat základní kapitál vytvořený z vkladů a základní kapitál vytvořený ze zisku.

Jak zjistit náklady na cizí kapitál

Náklady na cizí kapitál:

Náklady kapitálu, které firma získá formou dluhu Rd (např. formou úvěru, emisí obligací), se vyjadřují v podobě úroku sníženého o daňový štít, tedy o úspory z daní, které z použití cizího kapitálu plynou, tedy: Rd= i (1 – t), kde i je úroková míra z dluhu, t je sazba daně.

Co je to pracovní kapitál

Každá firma by měla mít tolik oběžného majetku (zásob surovin, materiálů, hotových peněz, pohledávek), kolik hospodárný provoz podniku vyžaduje, tento majetek se souhrnně nazývá pracovní kapitál.

Co je cizí kapitál

Cizí kapitál je kapitál firmy, na který si daná společnost musela půjčit. Jde o závazky: např. úvěry u bank, závazky vůči dodavatelům, finančnímu úřadu, zaměstnancům a podobně. Bývá označován jako cizí zdroje.

Jak zvýšit vlastní kapitál

O zvýšení základního kapitálu rozhoduje valná hromada dvoutřetinovou většinou všech hlasů společníků (nevyžaduje-li společenská smlouva poměr vyšší) a musí být o tom pořízen notářský zápis. Jednatelé jsou povinni bez zbytečného odkladu podat návrh na zápis zvýšení základního kapitálu do obchodního rejstříku.

Co obsahuje rozvaha

Rozvaha je účetním výkazem, který obsahuje uspořádaný přehled majetku podniku, z hlediska struktury podnikových aktiv a pasiv v určitém ocenění k určitému datu, k tak zvanému rozvahovému dni, resp. ke konci rozvahového dne (pokud se jedná o účetní závěrku mezitímní i k jinému datu).

Jak stanovit náklady vlastního kapitálu

Obecně lze náklady na vlastní kapitál určit buď na bázi tržních přístupů nebo metod a modelů vycházejících z účetních dat. Základními metodami, které se používají pro odhad nákladů vlastního kapitálu, jsou: model oceňování kapitálových aktiv – CAPM. arbitrážní model oceňování

Co je kapitálová potřeba

Částka kapitálu, kterou musí mít banka nebo jiná finanční instituce, jak požaduje její finanční regulátor.

Jak se počítá pracovní kapitál

Pracovní Kapitál = Zásoby + Pohledávky – splatné faktury.

Co patří do dlouhodobého kapitálu

Dlouhodobý cizí kapitál:

tvoří dlouhodobé bankovní úvěry (např. hypoteční), emitované podnikové obligace a dlužní úpisy, leasingové dluhy a jiné dlouhodobé závazky.

Co patří do cizích zdrojů

cizí zdroje financování, v rozvaze se řadí mezi pasiva, jde o závazky: např. úvěry u bank, závazky vůči dodavatelům, finančnímu úřadu, zaměstnancům a podobně. Naopak tedy nejde apriori o majetek, aktiva. Cizí kapitál někdy též označován jako „cizí zdroje“.

Jak se uctuje základní kapitál

O základním kapitálu budeme účtovat ve skupině 41 (obvykle na účtu 411). Na oddělených analytických účtech je potřeba sledovat základní kapitál vytvořený z vkladů a základní kapitál vytvořený ze zisku.

Proč se snižuje základní kapitál

U snížení základního kapitálu je kladen primární důraz na ochranu věřitelů společnosti. Ustanovení o ochraně věřitelů se nepoužijí, snižuje-li společnost základní kapitál za účelem úhrady ztráty. O zvýšení či snížení základního kapitálu rozhoduje valná hromada svým usnesením.

Co patří do aktiv v rozvaze

Aktiva představují v účetnictví všechno, co účetní jednotka vlastní a v budoucnu jí to přinese ekonomický prospěch (tj. například majetek, zásoby, peníze, licence, …). Opakem aktiv jsou pasiva, která představují závazky, vklady vlastníků do společnosti, zisky (ztráty) minulých let a výsledek hospodaření běžného roku.

Co kam patří v rozvaze

Tento finanční výkaz podává přehled o majetku podniku (aktivech) a zdrojích jeho krytí (pasivech) v peněžním vyjádření k určitému datu (rozvahovému dni) a umožňuje tak posoudit finanční postavení podniku. Rozvaha se proto také někdy nazývá výkazem o finanční pozici.

Jak se dělí Obezny majetek

OM se člení na: zásoby, pohledávky, finanční oběžný majetek.

Co tvoří pracovní kapitál

Každá firma by měla mít tolik oběžného majetku (zásob surovin, materiálů, hotových peněz, pohledávek), kolik hospodárný provoz podniku vyžaduje, tento majetek se souhrnně nazývá pracovní kapitál.

Jakou podobu může mít kapitál

Nazývají se také kapitálové statky. Kapitál může nabývat různých podob a významů. Jsou jím věcné statky, výrobní prostředky, peníze, cenné papíry, ale i patenty a licence, které přinášejí svému vlastníkovi zisk ve formě úroků, podílu na zisku, dividend apod.

Co patří do cizího kapitálu

cizí zdroje financování, v rozvaze se řadí mezi pasiva, jde o závazky: např. úvěry u bank, závazky vůči dodavatelům, finančnímu úřadu, zaměstnancům a podobně. Naopak tedy nejde apriori o majetek, aktiva. Cizí kapitál někdy též označován jako „cizí zdroje“.

Co spadá do ciziho kapitalu

Patří sem krátkodobé bankovní úvěry, dodavatelské úvěry, zálohy přijaté od odběratelů (odběratelské úvěry), půjčky, částky dosud nevyplacených mezd a platů (závazky k zaměstnancům), nezaplacené daně, výdaje příštích období, dlužné dividendy.